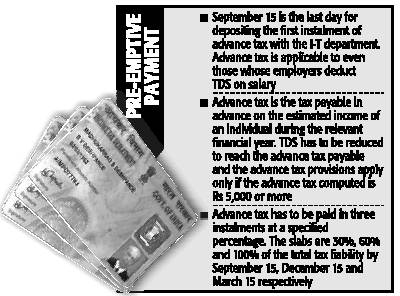

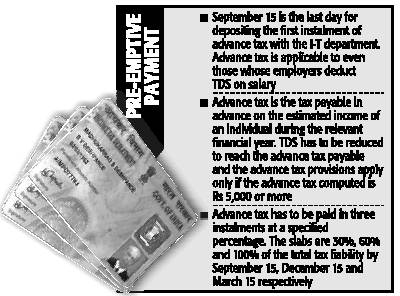

Are you salaried? If yes, do you know September 15 is the last day to deposit the first installment of advance tax with the I-T department? It applies to you even if your employer deducts TDS on salary, say Vishal Malhotra and Alok Vasant from Ernst & Young...

RAJESH Mehta is a salaried individual. He earns interest income of Rs 15,000 in a year from various sources such as bank deposits, small-saving schemes, bonds and others, against which no tax has been deducted at source. The incremental tax liability, considering that he is in the highest tax bracket, comes to Rs 5,050. Rajesh is liable to pay advance tax of Rs 1,520 by September 15, Rs 1,510 by December 15 and Rs 2,020 by March 15 failing which he would be burdened with an interest liability of Rs 310 (approximately).

Overview

An individual is taxed on the income earned by him during a financial year (From April 1 to March 31 of the next year). The discharge of tax is primarily by way of tax deducted at source (TDS) and payment of tax by the individual as ‘advance tax’ and ‘self assessment tax’. Advance tax is the tax payable in advance on the estimated income of an individual during the relevant financial year. Tax deducted or deductible at source is required to be reduced to arrive at the advance tax payable figure and the advance tax provisions apply only if the advance tax so computed is Rs 5,000 or more. Individuals are required to pay advance tax in three installments at a specified percentage - 30%, 60% and 100% of the total tax liability by September 15, December 15 and March 15 respectively. Default or shortfall in payment of the advance tax attracts penal interest. Payments are required to be made through designated banks by using prescribed challans (ITNS 280). Since the requirement to attach the challans along with the tax returns has now been done away with, it is important to mention the Permanent Account Number (PAN) correctly in the challan and fill in the relevant reference number allotted by the bank in the tax return.

Applicability To Salaried Employees

For a salaried employee with no other significant income, the advance tax provisions had little relevance till about a year back since the entire tax on his salary income was being discharged by way of TDS by his employer and there was generally no advance tax liability. This was because the individual’s interest earnings from bank deposits, NSCs, specified bonds/debentures and other securities to the extent of Rs 12,000 to 15,000 were not taxed thanks to the provisions of section 80L of the I-T Act. However, the Finance Act 2005 omitted this section with effect from the financial year 2005-06. Compliance of the advance tax provisions tends to present a greater hassle than the actual payment.

But there is a way out. Section 192 of the I-T Act, dealing with TDS on salaries, permits an employee to furnish a statement of other incomes that he is likely to earn in the year to his employer. Where such a statement is furnished, the employer is required to accordingly increase the TDS on the salary payments by taking into account the additional income of the employee. This saves the individual from advance tax compliance—computation, payment by due dates and so on. So be sure to provide your employer with these details, as it will save you a lot of hassle.

Courtesy: The Economic Times, Bangalore : September 12, 2006: available at Beware taxpayers: Ides of September cometh